ECONOMIC OVERVIEW: GDP growth in FY24 beats estimates; domestic economy resilient

As of the quarter that ended in March 2023, India's real GDP rose by 6.1% year over year, compared to 4.4% growth in the preceding quarter and 4.1% growth during the same period the previous year. The GDP grew by 7.2% overall in FY-23, exceeding market expectations. Due to high rates of inflation, the private sector's consumption saw subdued development, while the services sector—which included the rise of trade, transportation, and lodging—led economic growth. Building on a 4.5% year-over-year expansion, the manufacturing sector also contributed to the quarterly rise. As compared to FY-23, inflation is predicted to decline in FY-24, which is good news for the outlook for household consumption.

Following a five-month peak of 1.72 lakh crore in October GST collections levelled out in November and December at 1.67 to 1.64 lakh crore.

OVERVIEW OF INVESTMENTS: Strong quarterly PE inflows; Office sector takes the lead again

INR 158.5 billion (USD 1.92 billion) was the amount of investment activity reported in Q2 that was 63% more than the previous quarter's activity and 60% more than the activity recorded in Q2-22. With the acquisition of operational assets in Hyderabad, Mumbai, and Delhi NCR accounting for about 65% of the total quarterly PE flows, the office segment reclaimed its title as the "most preferred asset class." Large, mature office assets in these locations with a single owner are the focus of these purchases. Nearly 84% of the investment flows were made by foreign investors, with the majority coming from institutions based in Singapore, Canada, and the USA. In Q2-23, Nexus Select Trust, India's first retail REIT, went public. It raised over USD 390 million (INR 32 billion) from the sale of its shares in May 2023.

Limited fundraising effort in Q2 and H2-23, with an office-focused fundraise

A total of USD 304 million was raised in the second quarter with a focus on the residential and L&I sectors. A total of USD 912 billion in fundraising initiatives aimed at the office sector were revealed throughout the quarter. Two significant institutional players that intend to concentrate on expanding their current commercial asset portfolio in the next years are primarily responsible for this. A major portion of the USD 30.4 billion financing round, which was announced by a well-known international real estate investment firm, is anticipated to be invested in the logistics and data centre industry in the Asia-Pacific area, particularly in India.

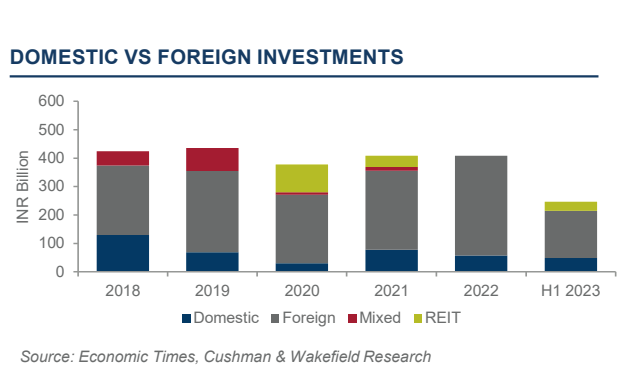

This year, office REITs and InvITs are anticipated.

By the end of the year, a new office REIT with a total of 45 million square feet is anticipated, created by a group of well-known asset owners, following the triumphant listing of India's first retail REIT. Delhi NCR-based NDR Warehousing is listing its approximately 19 million square foot portfolio across India in order to evaluate their first INR 2,000 Cr InvIT.

Corporate Real Estate Transactions

Corporate transaction volumes for the quarter totaled INR 21.4 bn (USD 260 million), over twice as much on a quarter-over-quarter and year-over-year basis. The average deal size increased to INR 129 million from INR 89 million in Q1 2023, which was a major contributing factor.

In 2022, there were quarterly average investments of INR 146.3 Mn over 347 projects, or 87 deals every quarter.

This quarter's top two cities for the percentage of all corporate space occupied are Mumbai (46%) and Pune (31%).

OVERVIEW OF INVESTMENT: Residential continues to gain traction while the office sector remains dominant

With INR 149.4 bn (USD 1.79 bn) in investment activity during Q4, it was around 66% more than Q4-22 and 2.8 times higher than the previous quarter's slower activity. After a lapse, offices emerged as the most favoured asset class in terms of sector share, with the largest proportion of 49% in quarterly inflows.

The residential sector came next, with a 28% share. At almost 73% of the overall quarterly inflow, foreign investors were mostly investing in the office and residential sectors.

Investments for the full year 2023 totaled INR 454.3 bn (USD 5.5 bn), 11% more than 2022 inflows, demonstrating the strength of the Indian real estate sector.

In 2023, the office sector remained dominant with a nearly 46% share, followed by the logistics and industrial (L&I) and residential segments, each with a 15.7% share. Investments in alternative sectors—hospitality, data centres, and real estate and infrastructure—rose to USD $1 billion in 2023 from less than USD 0.5 billion during the preceding five years, accounting for a sizeable 9.61% of all investments. The percentage of foreign investors was only 67% in 2023 as opposed to a significantly greater 85% in 2022, mostly because of the dangers associated with geopolitical tensions. Singaporean investors had the biggest percentage (26%) followed by American investors (14%).

The residential sector came next, with a 28% share. At almost 73% of the overall quarterly inflow, foreign investors were mostly investing in the office and residential sectors.